FinTech

2025

From Uncertainty to Confidence: American Express Trip Cancel Guard

I owned the full design process end-to-end — from leveraging user research data and synthesizing insights, through wireframing, prototyping, to final hi-fi delivery and engineering handoff. The PM defined business scope and success metrics. I defined the experience strategy and all interaction decisions. Legal and compliance review was iterative throughout, not a gate at the end.

Research

What I learned before designing anything

Before touching Figma, I dug into why the existing TCG product underperformed. The core finding wasn't what we expected — it wasn't primarily a pricing problem. It was a trust and comprehension problem.

Problem area

Buy-now-or-never protection chaos

The original TCG product had a fundamental structural problem: it could only be purchased at the exact moment of booking standalone flights through AmexTravel.com. No post-booking additions. No third-party bookings. No packages. The tight constraints made it functionally irrelevant to most cardholders' real travel behavior.

No pricing transparency before commitment

Users were asked to decide on a product without knowing its price until deep into a purchase flow. Insurance decisions require cost information upfront — every user session confirmed this.

Design goals

What I aimed to achieve

Build confidence through transparency

Show price and coverage before asking for commitment. Reduce the cognitive friction that was causing users to defer — and never return.

Design decision 01

Focusing on what travelers actually care about

Research showed cardholders want simple, flexible protection — not a feature list. The redesign let cardmembers add coverage after booking flights anywhere (not just the Amex portal), with clear 75% reimbursement for any reason up to 2 days before departure.

This was a direct trade-off: prioritizing real-world flexibility over the legacy restriction. The product team carried the business case for expanding the purchase window; my job was to make the expanded access feel natural and trustworthy — not a workaround.

Top Benefit Highlights

Flexible addition window

Add protection even after booking

Any-reason coverage

Cancel up to 2 days before departure

Clear reimbursement

Up to 75% of non-refundable costs

Exclusive AMEX perk

Available only to cardholders

Design decision 02

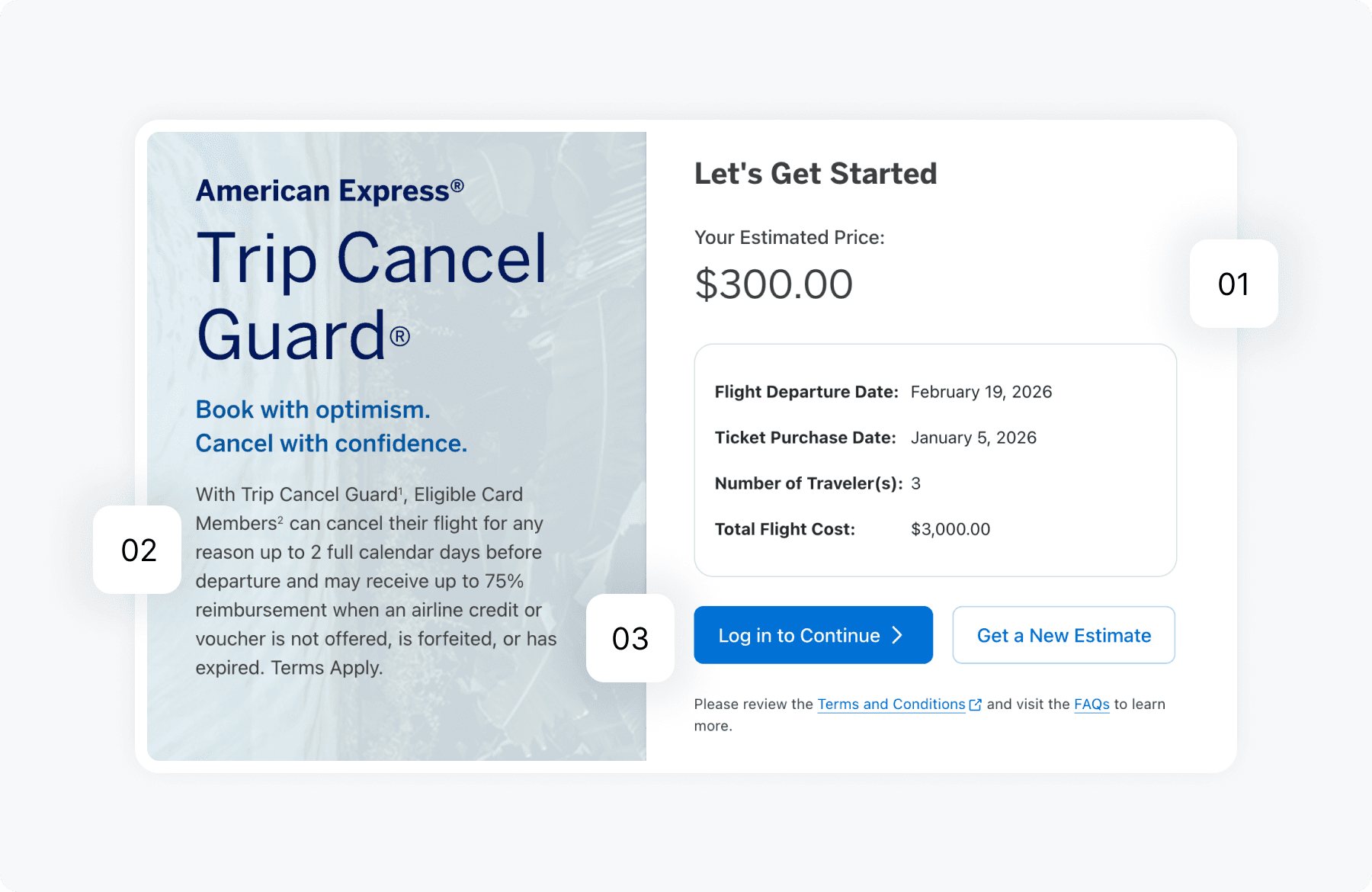

Building trust through a preview & quick quote mode

Many cardholders hesitate because they don't know the cost before starting a purchase flow. Rather than pushing for immediate commitment, I introduced a Preview & Quick Quote Mode — an instant personalized quote generated before any login or purchase intent is required.

1. Quick Quote generator

It reassures cardmembers by letting them see exact pricing and coverage instantly without any risk or login pressure.

Design decision 03

Turning the final step into a confident confirmation

The original checkout page treated every logged-in cardholder as a stranger. The redesign started with one principle: don't ask for what Amex already knows. For a logged-in Gold cardholder, that meant arriving at checkout with name, DOB, flight details, address, email, and billing card already populated — ready to review, not re-enter.

This was a direct trade-off: defaulting fields to blank for compliance safety versus surfacing pre-filled data from the cardholder's profile. The payments team confirmed card-on-file could be surfaced without re-authentication under a defined threshold. My job was to make that feel like recognition, not assumption.

Purchase Journey After Login

What the cardholder sees on arrival

Trip details pre-populated

Flight departure date, ticket purchase date, and destination pulled directly from their booking — no re-entry required.

Card on file, ready to charge

Billing card and address surface automatically. One less decision at the highest-stakes moment.

Traveler identity confirmed, not re-entered

Name and date of birth of primary card holder arrive pre-filled from the cardholder profile — editable if traveling on behalf of someone else.

Security code as an intentional gate

A deliberate, non-negotiable signal that the cardholder is present and authorizing — retained from the payments security team's requirements.

Constraints Navigated

The real-world friction that shaped every decision

Design at American Express doesn't happen in a vacuum. Working within a large financial institution meant navigating a set of constraints that shaped the solution as much as user research did. These weren't obstacles — they were part of the design problem.

Stakeholder → Product description and quick quote tool both required above the fold

The business stakeholder required both a product description and quick quote tool visible in the hero without scrolling — risking a cluttered experience that undermined the clarity-first direction. Resolution— Designed a two-column hero layout with the product description on the left and the quote tool on the right. Both lived above the fold without competing, giving users just enough context to act.

Retrospective

Designing for trust and confident decisions

Before and After redesign

Impact

Clarity That Converts

High-intent traffic (~18.7K visits month one) with strong signal that users were actively evaluating coverage value before committing — the 20.5% estimate-to-continue rate validates the Quick Quote approach.

Accessibility Compliance

Made sure all interactive components met WCAG 2.1 AA standards and satisfied Amex's legal and compliance requirements. In the final stage before the site went live, I partnered directly with QA to validate accessibility across the full experience.